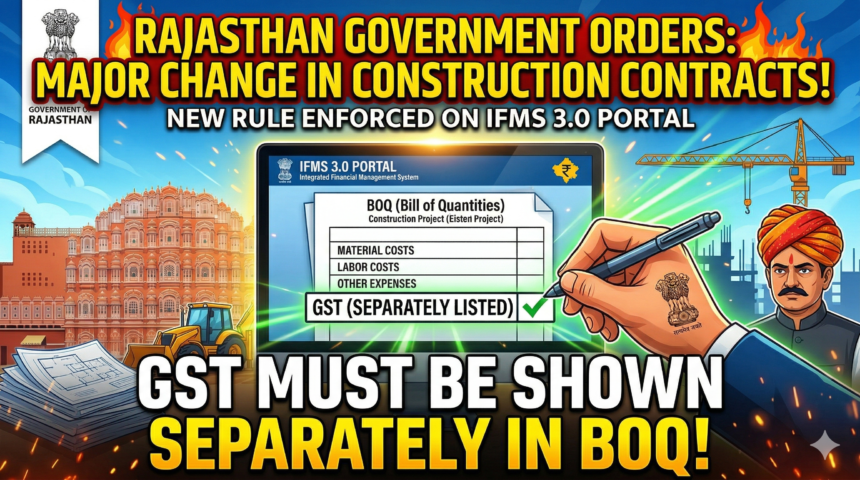

Jaipur, Rajasthan – In a major administrative reform aimed at increasing transparency and reducing financial irregularities in public construction contracts, the Rajasthan Finance Department has issued a directive requiring the Goods and Services Tax (GST) to be displayed separately in the Bill of Quantities (BOQ) under the IFMS 3.0 portal. The new system will take effect from April 1, 2026.

📊 What’s the Change?

Under the new rule, all construction departments across the state must prepare the Basic Schedule of Rates (BSR) without GST and upload it into the government’s Integrated Financial Management System (IFMS 3.0) — the online financial management platform used by the Rajasthan government. BOQs generated during tendering will now be shown “exclusive of GST,” clearly separating the base cost and the tax amount.

Until now, many tenders and cost estimates included GST within the overall rate, making it difficult to judge the actual cost of work and often creating opportunities for manipulation. The new rule aims to remove these ambiguities and curb corruption and cost distortions in contract awards and billing.

🛠️ How It Works

- GST‑free BSR: Departments must create and upload the BSR excluding GST, so that BOQs reflect only the base cost of work.

- Separate Tax Display: During the tendering process, GST will be added at applicable rates and shown separately, rather than being bundled into unit prices.

- Sanction and Billing Stage: When generating sanctions and processing bills, departments will calculate the gross payable amount and then add GST as a separate line item according to current tax rates.

📅 Transition for Existing Projects

For projects and tenders that were initiated before April 1, 2026, the old GST‑inclusive BSR will still be available for reference to avoid confusion in ongoing work. The new GST‑separation rule applies to all new estimates, tenders, and contracts created after the implementation date.

📈 Expected Impact

Officials say this reform will make government infrastructure spending more transparent and fair, giving contractors a clear understanding of how tax is applied and helping authorities better monitor public expenditure. It is also expected to reduce opportunities for under‑the‑table adjustments and disputes related to tax calculation in government contracts.

Departments have been urged to strictly follow the revised procedure and contact the IFMS project office if they encounter any technical issues.